©ROMOLOTAVANI/ISTOCK/THINKSTOCK

A reduced corporate tax rate, such as the one proposed by President Trump, is an obvious win for corporations. For asset-intensive companies, a reduction in the corporate tax rate can also provide a one-time cash flow opportunity. Let’s explore how.

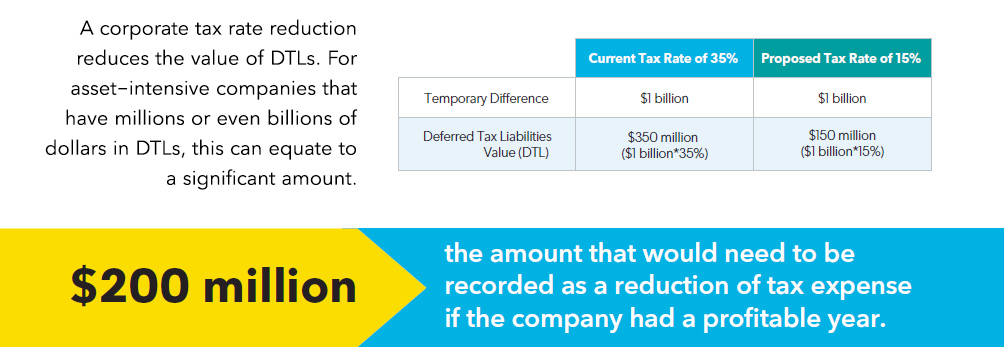

Asset-intensive organizations often have millions or even billions of dollars tied up in deferred tax liabilities (DTLs), and in many cases a substantial portion is attributed to fixed assets depreciation. Generally, tax depreciation does not impact a company’s effective tax rate (ETR) since it is a timing difference. But a reduced corporate tax rate means as the value of DTLs go down, income and earnings per share increase. For asset-intensive companies that have millions or even billions of dollars in DTLs, this can equate to a significant amount.

As an example, consider a company with a temporary difference of $1 billion, from a prior year, but is expected to reverse in future years. The DTL at the beginning of 2017 was $350 million, based on the 35 percent tax rate in effect as of December 31, 2016 ($1 billion * 35 percent). Assuming that legislation is enacted on December 20, 2017 that reduces the tax rate from 35 percent to 15 percent, the value of DTLs as of December 31, 2017 would be $150 million ($1 billion * 15 percent). As a result, DTLs would be reduced by $200 million ($350 million value in 2016 - $150 million value in 2017). The entire $200 million difference would need to be recorded in the 4th quarter as a reduction of that quarter’s tax expense.

If a company is not prepared for such a large tax reduction expense, this scenario could have a negative impact on their bottom line. However, if the company takes a proactive approach and identifies ways to accelerate depreciation before their DTLs are revalued at a lower rate, they may see a permanent tax expense benefit.

Rather than take a wait and see approach and react to whatever tax reform is ultimately passed, financial and tax executives should explore available options. This will require sophisticated analysis along with sophisticated technology to accurately compare the impacts tax law will have on past, current (both actual and proposed), and future tax strategies. Whether a company relies on their in-house analysis capabilities or third-party solutions, it is imperative that they identify the steps necessary to stay ahead of tax reform, and maximize tax cash.

Diane Tinney is the Director of Product Management at Bloomberg BNA, Software.