By Sarah Ovuka & Dianora Aria De Marco

The Revenue Recognition Working Group (RRWG) of FEI’s Committee on Corporate Reporting (CCR) met in early December to discuss the latest technical updates and to share implementation insights as many approach the finish line in implementing the new revenue recognition standard. The group discussed various topics of interest and held a general Q&A session with representatives from the Big Four accounting firms, the FASB, and the AICPA.

Topics of Interest

Remaining Performance Obligations Disclosure

The RRWG discussed the common challenges many companies are facing in preparing the disclosure requirements for remaining unsatisfied performance obligations. Specific challenges discussed related to the amount and nature of the information needed to prepare this disclosure, particularly given the significant judgments and estimates involved in determining when remaining performance obligations are expected to be satisfied and how to allocate the transaction price to the remaining performance obligations. The RRWG also discussed the significant work required from a systems readiness perspective, emphasizing that companies will have to review the requirements of the disclosure closely and assess whether their systems are capable of accumulating the associated data.

Investor Relations Considerations: The group discussed points to consider when reviewing this disclosure with Investor Relations, particularly with respect to benchmarking any such discussions to current disclosures of backlog. Companies should consider whether they have historically disclosed backlog, and if so, whether the previously disclosed backlog measurements align to the requirements to disclose information about remaining unsatisfied performance obligations under ASC 606. For some companies, backlog is historically a manufacturing term (i.e. hardware in process) and not necessarily representative of what will be considered unsatisfied performance obligations under the new guidance. Therefore, the RRWG discussed that clear messaging on this disclosure will be critical.

Practical Expedient: The RRWG also discussed the practical expedient that would allow companies to forego the remaining performance obligations disclosure for any of its contracts that have an expected duration of one year or less. The group emphasized the importance of deciding to use a practical expedient as soon as possible and to think carefully through the process of operationalizing such an election. While the practical expedient is intended to simplify the process, many companies shared the experience that implementing the expedient actually complicated the process. Therefore it was discussed that companies electing the referenced practical expedient should exercise caution when implementing it. For example, one common pitfall may be assuming that the short-term deferred revenue balance is representative of the contracts that could be excluded by this practical expedient. In reality, much of the short-term deferred revenue could be related to contracts with an original duration greater than one year. Therefore the assessment to exclude short duration contracts through the use of this practical expedient should be assessed carefully at the contract level.

Other Considerations: The RRWG discussed various other considerations affecting the operationalization of this key disclosure, such as benchmarking practices used to estimate future recognition of performance obligations and the impact of termination penalties and provisions on the determination of the contract duration and performance obligations. There was also discussion around the various estimates involved in the determination of the transaction price (e.g. variable consideration, applying the constraint, etc.) and the impact they have on preparing this disclosure. There was also emphasis on the importance of system readiness, including considerations to the consolidation process and the varying state of progress of contracts across entities.

SEC Comment Letters

The RRWG discussed the SEC comment letters issued to date on ASC 606. Three early adopters received comment letters related to the following areas of the guidance:

- Accounting for sources of variable consideration, including refund liabilities and reassessment of variable consideration

- Accounting for rebates paid to customers

- Disclosing the nature of changes in contract balances, including how the timing of payments and satisfaction of performance obligations impact contract assets and liabilities

- Substantiating the method used to recognize revenue on over-time performance obligations

- Determining that costs obtaining a contract are incremental and thus eligible to be capitalized

- Determining of the appropriate amortization period for commissions costs, with consideration to contract renewals

- Disclosing remaining unsatisfied performance obligations

The SEC also issued comment letters addressing SAB 74 disclosures, specifically asking companies to disclose a quantitative impact, if available, of adopting the new standard. Included in the RRWG meeting materials was an

FEI study on all SEC ASC 606 comment letters issued to date, which summarizes such correspondence in greater detail.

Statutory Reporting

The RRWG discussed the fact that the adoption of ASC 606 for consolidated reporting purposes may result in new or modified differences between statutory reporting and consolidated reporting. Companies operating in countries with the requirement to file statutory financial statements must understand which accounting standards may be applied in those respective jurisdictions and determine what new or modified differences may arise as a result of adopting ASC 606 at the consolidated reporting level. While no explicit scenarios were discussed, the group agreed this was a complex area to manage, and shared experiences and best practices to address this issue. Companies should keep this area on their radar as they finalize implementation efforts.

Communicating with Investors

Stacy Harrington, Microsoft’s Senior Director of Corporate Revenue Assurance, reminded the group of the importance of communicating the anticipated changes to the financial statements with investors throughout the implementation process. Similar to her presentation

Learning from the Leaders: How to Prepare Your Investors for the New Revenue Standard (see presentation beginning at roughly 34 minutes into the recording) at the second annual

Pacesetters in Financial Reporting Conference, Stacy shared key actions Microsoft took in early adopting ASC 606, and shared their timeline and some best practices with the group:

- Microsoft communicated a clear timeframe of when information would be provided to analysts.

- On August 3, the same day Microsoft filed an 8-K disclosing the company’s election to early adopt the new revenue (and lease) standard, Microsoft held MFST New Accounting Standards and FY18 Investor Metrics Conference Call, in which management described the results under ASC 605 and detailed how an analyst could translate the impact of ASC 606.

- Microsoft’s accounting department proactively educated the Investor Relations (IR) department on the anticipated changes. For example, the accounting department helped compile a detailed Q&A document for IR to reference when answering questions from analysts.

The below timeline details Microsoft’s approach to adopting the new revenue standard, which includes details from the inception of their implementation planning through their issuance of Q1 results under ASC 606.

.png.aspx?lang=en-US) FEI summarized

FEI summarized Microsoft’s highlights and other tips for communicating the impact of ASC 606 to investors.

Accounting Firm Update

A representative from the one of the Big Four accounting firms provided an update on the latest ASC 606 trends observed by the Firms in their work in assisting companies to adopt the new standard. The Firm representatives shared that many issues have been addressed and that the Firms have seen a decline in the volume of new issues raised since mid-November. The remaining issues that are taking the most significant time and effort to address have generally been highly judgmental and fact pattern specific. A majority of these questions were related to principal versus agent considerations (reporting revenue gross versus net) and identifying performance obligations. There have also been many questions around disclosures, in particular around disaggregation and on backlog, as referenced above.

FASB Update

A representative from the FASB provided the RRWG with an overview of ASC 606 implementation to date.

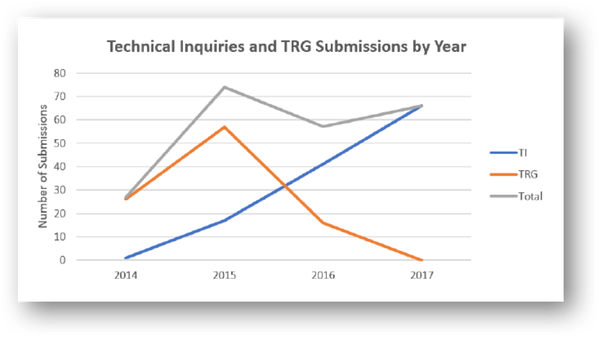

The below chart depicts the number of TRG submissions compared with the number of technical inquiries received since the issuance of ASC 606 in 2014. As the effective date approaches, questions have shifted from TRG submissions to technical inquiries.

The FASB also noted that the staff has been receiving more questions on specific fact patterns, and more questions from smaller public and private companies. They remarked that the shift in questions from large public companies to smaller public companies was encouraging in terms of overall market readiness of the standard. The FASB remains ready to assist companies throughout their implementation process.

AICPA Update

A representative from the AICPA provided a brief update on the work performed by the AICPA Industry Task Forces. Of the original 140 issues addressed by Task Forces, roughly 95% have been discussed by the Financial Reporting Executive Committee (FinREC). As of December 1, about 90% of the issues were out for exposure. Since the exposure process began, nosignificant changes have been made to the conclusions included in the exposure drafts.

The AICPA credited the successful process to having the Firms and the SEC involved throughout the related discussions. The next edition of the revenue recognition guide will be finalized in January 2018.

Final Thoughts

In 2018, calendar year-end companies will be operating under the new revenue standard.

SAB 74 disclosures have been a helpful indication of where companies are in their implementation process. We will continue to assess the impact of the new standard once effective for public companies in 2018.

Sarah Ovuka is Financial Executive International's Professional Accounting Fellow and Dianora Aria De Marco is FEI's Manager of Accounting Policy.