© Jirsak/iStock/Getty Images Plus

Not much more than seven months ago, the Securities and Exchange Commission (SEC) announced an important new 10-K disclosure requirement: to describe human capital resources and objectives or measures used in the management of the business that are material to the understanding of a company’s business.

But how?

Other than mandating the number of employees (an already existing requirement), the new principles-based rule leaves it to the company to apply considerable judgment in describing “any human capital measures or objectives that the registrant focuses on in managing the business.” It doesn’t even define human capital or managing the business. The omissions were intentional.

The goal, said Jay Clayton, then Chairman of the SEC, is “to elicit disclosure tailored to each company’s particular industry and business model while being flexible enough to continue to allow for fulsome disclosure as businesses evolve in the future.” (For more background, see How to Approach the SEC’s New Human Capital Disclosures.)

Faced with a blank canvas last August when the rule was announced, many companies formed cross-functional teams to consider, among other things, what information to disclose, the length of the disclosures and whether (and how) to include quantitative metrics. Of course, most companies wanted to avoid disclosing too little, or too much.

Our review of the 10-Ks of approximately 150 S&P 500 companies — filed from November 8, 2020, the rule’s effective date, through February 15, 2021 — paints an early directional picture of how companies incorporated the new requirement. While the results are a snapshot of only a portion of the S&P 500, the takeaways may prove helpful for future filings.

So where did this wave of first responders, representing 11 industry sectors, come out?

Our analysis revealed patterns in the nine major categories, or themes, of human capital disclosures on which industry sectors chose to focus. At the same time, we found broad differences among individual companies in the tools and treatment they used in presenting their disclosures.

To be sure, it’s still very early days in this new area, and evolution is a certainty, in large part because of intensifying interest from investors, who see human capital as a key driver of long-term value.

For now, though, here is what the once-blank canvas looks like.

Findings

The long and the short of it. Some filers provided only a single paragraph to describe their human capital resources. Some took as many as three pages. The average length was approximately one full page.

Qualitative versus quantitative. Companies had to decide how much of the disclosure should be narrative discussion and how much metrics. The majority of the early responders chose a mostly qualitative approach, with some employing a small number of metrics to underscore and explain one or more portions of the narrative.

About two-thirds included at least one metric in addition to the number of employees. Some included a breakout of employees by geography, the number of part- and full-time employees, the number or percentage of employees covered by collective bargaining agreements, or a breakdown by gender. Others included attrition rates and the results of employee engagement surveys, as well as injury incident rates, to share information associated with employee safety.

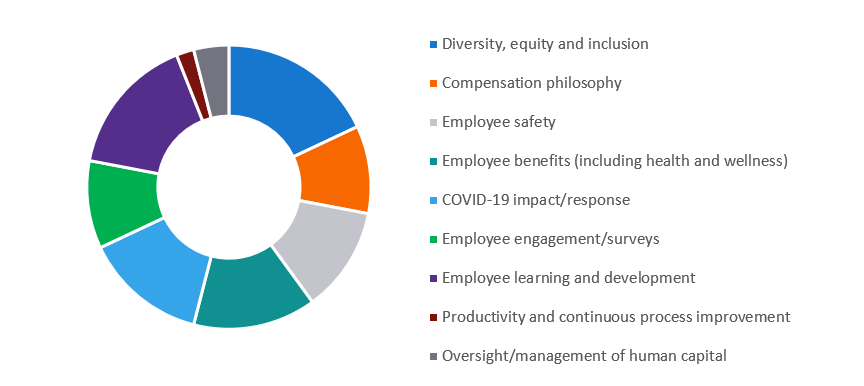

Key themes. The nine major themes that appeared in the filings are listed in the chart below — the bigger the slice of the pie, the more often that theme was discussed.

The most commonly discussed theme was diversity, equity and inclusion (DE&I). A majority of the filers submitted at least a qualitative discussion of this topic, with more than a quarter using a metric breaking down employees by gender and/or including figures about ethnic diversity. The frequent focus on this theme in part reflects investor concerns about diversity issues related to proxy voting and stewardship policies.

Other often-cited themes included:

- Employee benefits, especially as they related to attracting and retaining talent

- Employee learning and development, with many companies describing, in narrative form, training programs leading to enhanced skills and some adding a dollar amount for training investments

- Employee safety, highlighted in particular by companies with manufacturing and industrial operations, with some citing specific incident rates or safety goals and others describing higher-level policies and procedures

- Employee engagement/surveys, as a tool to evaluate employee satisfaction and identify areas for improvement, although most companies omitted specific findings

- COVID-19 impact/response, encompassing well-being, health and safety, as well as work-from-home arrangements

- Compensation philosophy, handled mostly at a high level

Industry patterns

Our review revealed a number of trends among industry sectors:

- Four topics were discussed by at least one company within every industry group: DE&I, employee safety, COVID-19 impact/response and employee learning and development.

- The greatest variability across industries involved discussions of compensation philosophy and employee engagement/surveys. Those two themes were discussed by about 80% of filers in the communication services and real estate industries, but by 0% in the materials and utilities industries.

- Across all industries, fewer than 40% of the filers disclosed oversight/management issues.

- On average, the greatest number of themes was discussed by companies in the real estate, industrials, energy, materials and communication services industries. The least number of themes, on average, was discussed in the utilities industry.

For more details about industry patterns and other aspects of our review, please see How do you value your social and human capital? Human capital disclosures findings from 2020 10-Ks.

What’s next?

The wide disparity in topics and treatment in the first wave of human capital disclosures is a natural consequence of a principles-based SEC rule. But given the potential for increased investor scrutiny, as well as ongoing regulatory interpretation, we expect these disclosures to evolve and be refined, with greater adoption of leading practices.

Already this year, investor pressure has ratcheted up, and the SEC has signaled that broader environmental, social and governance (ESG) disclosure is a priority. In response, we expect companies to enhance their ability to collect data and to consider further controls and processes in this area. It will certainly be interesting to continue monitoring human capital disclosures contained in the next wave of 10-Ks.

Marc Siegel is a partner with Ernst & Young LLP’s Financial Accounting Advisory Services (FAAS) practice and a member of the Sustainability Accounting Standards Board (SASB). The views expressed by the author are not necessarily those of Ernst & Young LLP or other members of the global EY organization.