Preliminary results of a joint survey between Financial Executives Research Foundation (FERF) and EY reveal that a majority of companies -- or 66 percent -- have initiatives to improve their financial statements and have incorporated the changes into filed statements. You can still take the survey here.

FERF and EY launched the survey on July 10th to better understand some of the initiatives that have taken place within organizations and to identify many of the benefits and impediments in moving forward with this important process. The survey results will culminate in a report due to be out in late fall 2015, which is intended to provide best practices for preparers, as well as, provide perspectives from audit committee members and the investor and financial statement user community.

The preliminary indications that suggest organizations are striving for improvement corresponds with data suggesting that certain companies’ financial statement word counts are dropping compared to previously filed reports.

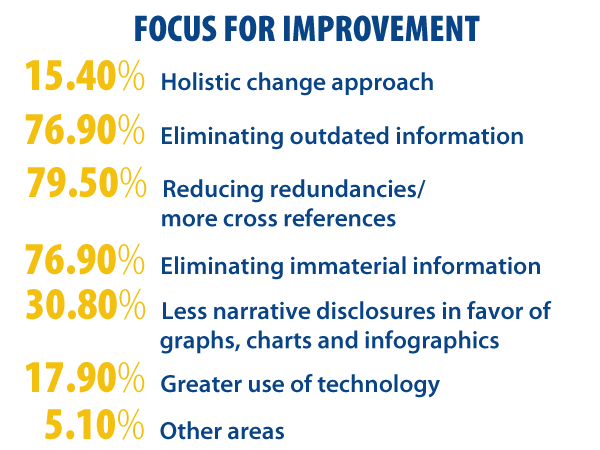

Organizations that have responded thus far seem to be focusing on three primary improvement areas. Reducing redundancies and eliminating outdated and immaterial information seem to be the greatest focus but it appears that companies are also taking a host of other actions to improve the way they communicate and report results.

The vast majority -- or 83% -- of those who have begun the improvement process are beginning with their annual and interim statements, as apposed to proxy statements or earnings releases.

The minority who, have not begun the process shared three primary reasons:

- they believe their financial statements already provide a reasonably good representation of their company’s financial standing and performance and are well-presented;

- they don’t believe that the investor community will benefit significantly; and

- they don’t believe that the benefits of the improved reporting do not justify the costs.

The majority or 57 percent believe that regulators and standard-setters are not doing enough to reduce complexity and increase the understandability of financial statements. As one participant indicated,

“Both SEC and FASB update existing literature to remove duplicate and irrelevant disclosure requirements. I know that projects are "underway" but these need to be a higher priority.”

Be a part of this important survey and report…share your experiences and views by taking the Disclosure Effectiveness survey. This survey will remain open only until August 7 so please act now.