As businesses evolve, the scope of the CFO’s role is expanding. CFOs now have to balance competing demands on their expertise, priorities and time, while often playing a transformational role in driving strategy for their business. These expanded responsibilities are creating a tension between the CFO’s financial and strategic roles. At the same time, this intensifies the need for more data to inform decision-making.

In this light, Grant Thornton’s 2017 CFO Survey looked at how more than 400 senior financial executives see the current state and the future of their business in the areas of risk, technology, investment and strategy. The survey also focused on identifying the challenges these executives face in adopting efficient solutions in these four areas. Of the survey respondents, 93% represent the middle market (companies up to $1 billion) and 92% are CFOs.

A range of industries were represented in the survey, with top respondents coming from manufacturing, nonprofit and financial services.

CFOs contribute to business strategy

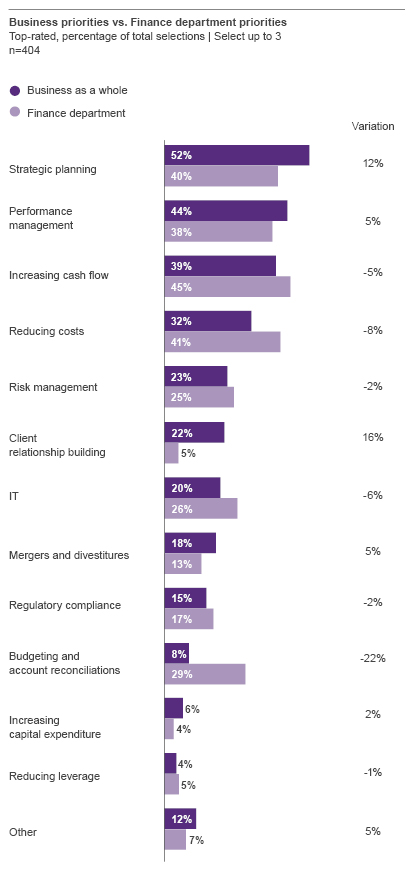

Given their expanding duties, today’s CFOs increasingly must balance their role of strategist across the business with their traditional CFO role. They reported a high level of involvement in strategy/executive committee meetings, and said they spend over one third of their time as strategic advisers. This is supported by the fact that strategic planning ranks third as a priority for the finance department, outranked only by increasing cash flow and reducing costs.

But for CFOs, investing in strategic planning is a trade-off that can reflect either a cost or an opportunity. For instance, many CFOs are getting involved with operating metrics — a step beyond the financial metrics they have traditionally used. Yet, whether this is an efficient use of their time or an imposition depends on the availability of analytical tools — such as analytics platforms — and on the CFO’s flexibility to do analytical “what-if” analyses.

So, if strategic planning is a top priority, the finance function needs to invest in its people and in the technology necessary to support business processes, such as budgeting, forecasting and long-term planning. This planning effort is not only related to financial data, but also to the operational information that drives the business. It starts with defining key business metrics and then tying these metrics to how they affect or drive bottom-line performance.

Graham Tasman, principal in Grant Thornton’s Business Consulting and Technology practice explains the current situation further: “Finding a solution to competing demands on the CFO presents an opportunity for innovation. The tension that the CFO is experiencing between priorities inside and outside of the finance function increases the need to streamline processes through technology, which, in turn, promotes more integration between finance, risk, treasury, and operations. Another improvement focus is to consider core versus non-core finance activities, leveraging shared services for non-core processes, while leveraging technology and data analytics for core activities that help focus limited resources on delivering the highest value for the business.”

Looking for more insights? Grant Thornton’s 2017 CFO Survey features additional insights into what the future looks like for CFOs. Click here to learn more.