The Securities and Exchange Commission’s Accounting Quality Model, a.k.a. Robocop, is a potential game changer for the SEC and for filers of XBRL. The SEC now has the ability to electronically examine each and every file submitted through the EDGAR system looking beyond XBRL acceptance to patterns or anomalies that could trigger closer inspection by SEC enforcement teams. In this article, we will examine what the Accounting Quality Model is and what is its purpose. We will also look at the steps preparers should take given the SEC’s analytical approach filed data.

Who is Craig Lewis and what is the Accounting Quality Model?

Craig Lewis joined the SEC as Economic Fellow in 2011 and soon after was appointed Chief Economist and Director of the Division of Risk, Strategy, and Financial Innovation. Dr. Lewis came to the SEC from Vanderbilt University with a charge to improve the SEC’s use of data. To that end, he created several new approaches to data within the SEC. In his own words,

“The Division of Risk, Strategy and Financial Innovation, or “RSFI”, was formed, in part, to integrate rigorous data analytics into the core mission of the SEC. Often referred to as the SEC’s “think tank,” RSFI consists of highly trained staff from a variety of backgrounds with a deep knowledge of the financial industry and markets.”

In order to accomplish the core mission, Lewis and his team created risk assessment models, a data warehouse and a set of risk assessment tools to analyze the data. One of the many outcomes from his work is the Accounting Quality Model.

What is the Accounting Quality Model?

Dr. Lewis indicated in one of his speeches that “At its core, AQM is a structured analytic model that takes flier information and identifies outliers and things that stick out by the type of disclosures being made and uses that data as a means to better understand our (SEC) filer space.” It should be noted that the AQM was not named the Accounting Fraud Detector, although it does play a role in identifying high risk companies.

Lewis goes on to describe the functionality and purpose of the AQM

“As you know, the SEC has a veritable treasure trove of information from various registrant filings. We are mining that rich vein of information and are applying the same quantitative approach to develop various ways to evaluate registrant filings and search for potential areas of risk. While we have several projects in development, we are particularly excited about what we call an “Accounting Quality Model” (AQM). This model is being designed to provide a set of quantitative analytics that could be used across the SEC to assess the degree to which registrants’ financial statements appear anomalous.”

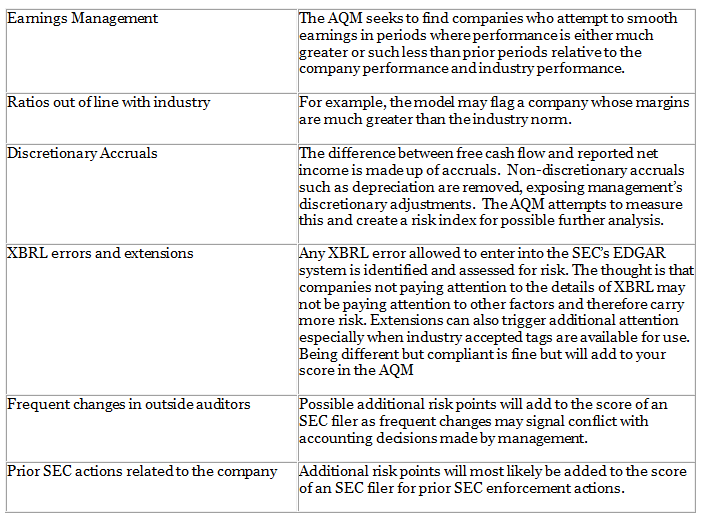

So what exactly does the AQM look for? Although the SEC will not specifically say, here are a few possibilities:

Once an overall number or rating is established for each return, the return may be referred to an appropriate division within the SEC for further review.

Although the AQM has already led to at least seven SEC actions for fraudulent activities, Lewis insists that the model is not designed specifically to detect fraud. Rather, the AQM’s goal is to improve the quality of financial information reported to the SEC by allowing the regulator to comment more quickly and comprehensively about reporting that needs improvement.

The SEC does not, according to Lewis, intend to publish the criteria within the AQM that leads to a high risk score. The “special sauce” will remain an evolving secret as the SEC identifies reporting tendencies both good and bad filings.

What are the XBRL filing Implications?

Here are a few things to keep in mind when filing with the SEC: 1. The quality of your XBRL counts. Mistakes and errors will lead to higher risk scores and subject your company to higher levels of scrutiny. 2. The tags you choose for your XBRL filings count. If you choose to create your own extension tag that says that you think your company’s reporting is different. If you are different, then the SEC may want to know why. 3. What you do not choose also tells the SEC something about your accounting. For example, if all your industry cohorts choose the same revenue tag and you don’t, they will be able to see that right away and it may lead to further analysis. This doesn’t mean you are wrong, it just means that you are different and the SEC will want to know why. 4. The SEC will also be parsing the words contained in detailed footnotes and management discussion and analysis in the near future. Word patterns matter and could give indicators about your company.

Author’s note: Craig Lewis resigned from the SEC on May 2, 2014 after three years with the SEC to return to his position at Vanderbilt University.

DataTracks US is part of DataTracks Services Limited, leaders worldwide in preparation of financial statements in EDGAR HTML, XBRL and iXBRL formats for filing with regulators. DataTracks prepares more than 12,000 XBRL statements annually for filing with regulators such as SEC in the United States, HMRC in the United Kingdom, Revenue in Ireland and MCA in India.

To find out more about DataTracks, visit www.datatracks.com or send an email to [email protected].