©PIOTR KRZEŚLAK/ITSOCK/THINKSTOCK

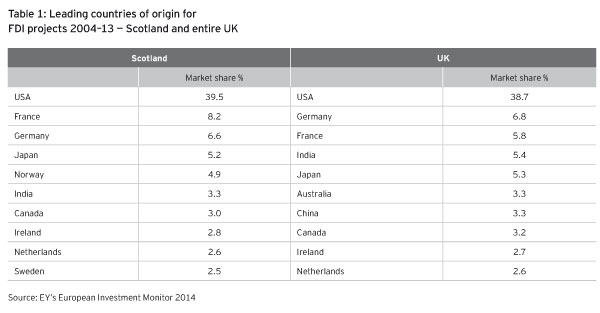

Scottish/American business ties are fairly deep and direct for both sides. The U.S. is the largest source of foreign direct investment (FDI) projects within Scotland, accounting for 41 percent of all investment projects, according to Scottish Development International (SDI) . In addition, SDI says, U.S.-owned companies also account for over 40 percent of Scottish business research and development expenditures.

On Thursday, more than 4.2 million Scots (97 percent of the adult population) will have a chance to vote on whether to remain part of the United Kingdom. Currently, Scotland has its own legal and education systems, but control of defense, borders and taxation remain with the U.K.

Here are three things U.S. financial executives need to consider if Scotland decides to go it alone:

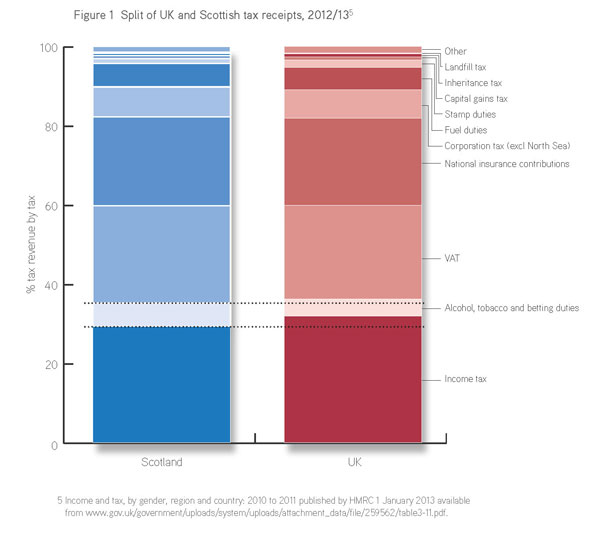

Taxes

As with any country, the key to corporate interest is defined by its tax structure.

Scotland currently follows the UK system for corporates, and that will likely continue for the near term following any independence move, according to the Institute of Chartered Accountants of Scotland.

“[The] way forward after a ‘Yes’ vote in the referendum is, in practice, to replicate the UK tax system for a transitional period (the number of years are not specified) with the potential for change in future,” according to a report issued by ICAS entitled Scotland’s Tax Future; Taxes Explained.

What happens after the dust settles and Scotland looks to compete with other domiciles for corporate tax revenue will depend a great deal on how much the possible new government in Edinburgh wants to compete with the UK and the rest of Europe.

© Institute of Chartered Accountants of Scotland

“A new tax border between Scotland and the rest of the UK means duplicating tax work and two tax authorities; corporation tax groupings fail to apply, loss and profit offsets will cease, taxable profits will be have to be allocated across borders, separate payrolls may be needed for employees in Scotland and the rest of the UK, VAT groupings, too, will cease,” the ICAS report says. “A flurry of corporate restructuring activity might then be expected after any ‘Yes’ vote, but in reality nothing can be implemented until the principles of any new Scottish system and its operations are [agreed].

Investment

U.S.-based companies remain the largest investors in Scotland, meaning U.S. companies on the ground should at least be considering how to respond to a “Yes” vote on Thursday.

In fact, Scotland has been more reliant on U.S. foreign direct investment than the UK as a whole, according to Ernst & Young’s 2014 UK Attractiveness Survey, with U.S. software companies at the top of the list.

“At a headline level, the number of FDI projects coming into Scotland in 2013 rose by 8 percent over 2012, with projects from the software industry and from the U.S. leading the way,” the EY report states. “Whilst the number of reported jobs from FDI projects in Scotland fell back for the second year running from its high point in 2011, the total FDI employment figure for the year was still above its average level over the past 10 years. "

© EY Scotland Attractiveness Survey

Despite these close ties, companies remain hesitant to put a post-independence plan together. A

KPMG survey released this summer said 84 per cent of Scottish firms that were questioned said they had not yet considered a continuity plan for how to deal with changes in regards to independence.

U.S. Disclosures

If Scotland were to vote “Yes,” U.S. companies with significant operations in the county -- or Scottish companies with U.S. subsidiaries in the U.S. -- will need to consider how they describe independence risk in regulatory disclosures.

Disclosures regarding issues that could arise due to the possibility of Scotland independence could be highlighted in a few locations, according to Don Whalen, general counsel and director of research for Audit Analytics in Sutton, Mass. That includes disclosures in a press release attached to a Form 8-K or in a company’s 10K as part of the M&A Risk Factors or M&A Results of Operations.

If a company files a press release to the SEC as an attachment to an Form 8-K, it would also, most likely, be on its website,” Whalen says. “Also, companies may address the issue in the Annual Reports provided to investors.”

Some of the larger Scotland-based financial services companies with U.S operations --such as Royal Bank of Scotland -- have already moved ahead with their disclosure through a “Political Risk” subsection of its Risk Overview portion of the annual report.

“Although the outcome of such referendum is uncertain, subject to any mitigating factors, the uncertainties resulting from an affirmative vote in favour of independence would be likely to significantly impact the Group’s credit ratings and could also impact the fiscal, monetary, legal and regulatory landscape to which the Group is subject,” the disclosure says.