A company that expands successfully into a new European market may be making money hand over fist. But when those foreign earnings are translated back to Dollars, much of their anticipated earnings and profit margin may vanish. What happened?

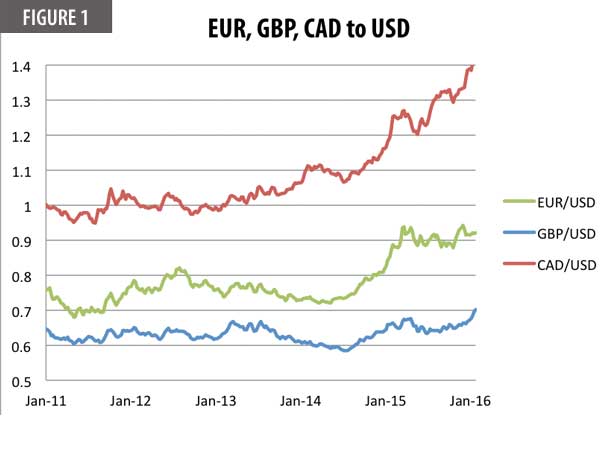

Substantial strengthening of the dollar began toward the end of 2014, and has continued through the beginning of 2016. Prior to this, foreign currency movement may not have been an issue for many U.S. multinationals. Why?

Substantial strengthening of the dollar began toward the end of 2014, and has continued through the beginning of 2016. Prior to this, foreign currency movement may not have been an issue for many U.S. multinationals. Why?

When the dollar was weakening against other currencies, the result of translating overseas earnings to Dollars was positive. In fact, the same amount of revenue translated to a weaker dollar actually resulted in higher revenue and better dollar margins. The irony, of course, is that as the dollar continued to strengthen over the past year, foreign earnings began looking worse for U.S.-based companies, and many started taking notice.

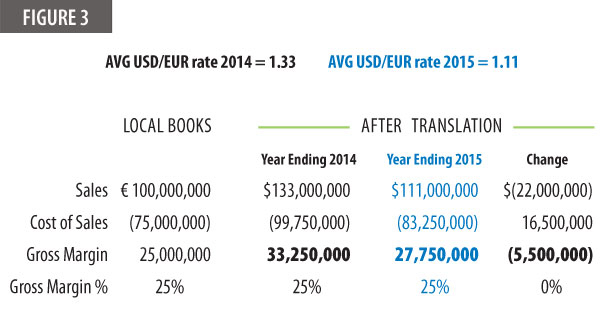

To illustrate, assume a scenario in which annual sales of a Euro (EUR) based subsidiary were €100M, cost of sales was €75M, and gross margin was €25M (25 percent). Using historical average EUR to USD rates for 2014 and 2015, these figures would translate to USD as follows:

As shown, both sales and gross margin Dollars look worse in 2015 when considering the change in EUR to USD rates, despite volume remaining flat from 2014.

As shown, both sales and gross margin Dollars look worse in 2015 when considering the change in EUR to USD rates, despite volume remaining flat from 2014.

Reduced margins and lower top-line revenues are resulting in confusion and questions from many investors and repeated, but necessary, explanations from CFOs during earnings calls. This often begs the question that if business is great overseas, why does it not look so great in the financials?

True, an astute analyst would look at ratios and observe that actual gross margin percentage remained unchanged as revenues and expenses would have been translated at the same rate. However, dollar margin and top-line revenues would appear lower as a result, and that makes a difference to some. Executives don’t like seeing margins that, despite remaining healthy (or perhaps even improved) overseas, look as if they’ve declined when translated back to the dollar.

What Can be Done?

For an in-depth article that answers this question and explores this topic further, please click on the banner below to gain aces to the entire article through FEIconnect.