How financial statement preparers can drive the disclosure effectiveness debate will be the subject at a panel at Financial Executive International's Current Financial Reporting Issues (CFRI) Conference in November at the New York Marriott Marquis.

FEI Daily spoke with Neri Bukspan -- a partner at Ernst & Young and featured speaker on an expert panel regarding financial disclosures at CFRI -- regarding the current environment and what CFOs and other financial executives need to consider.

FEI Daily: Where do you think many financial statement preparers stand on disclosure effectiveness? How much progress has been made compared to where the regulators want to see them?

Neri Bukspan: Most companies exploring disclosure effectiveness are doing it because they feel it's the right thing to do and it's an appropriate way for them to tell their story. And, frankly, there are no regulatory brownie points associated with it.

Most realize that disclosure simplification provides them an appropriate benefit by bolstering investor confidence and it enhances the look and feel of communications, while in some cases also introduces process efficiencies. It enhances their corporate image and appearance, and investors appreciate it and embrace it. It coincides with the evolution of the non-financial world from graphics, technology and media to present information in a more contemporary way than they've done in the past.

I have been very encouraged by the latest push for disclosure effectiveness because we haven't seen much done in the last two decades. There is a very encouraging movement by some very large companies that have significant market clout and a large investment base that proves that they are committed to doing it. To me it's an evolution, not a revolution, and the trajectory is quite impressive and favorable.

FEI Daily: Where are preparers getting most of their cues for how to present information? If it’s not coming from regulators, is it coming from investors?

Bukspan: Some discussions have been raised over the years by investors, other preparers and regulators who say, "Okay, this could be one way to do some things. This is going be a useful way to represent things, and this could be something you want think about." The SEC has clearly been on record encouraging companies by providing a ‘call to action’ for companies to ‘experiment’ and improve their disclosures and offered to discuss new approaches with registrants. In addition, audit committees and boards also serve as catalysts in many cases. This has been well documented, and we have completed our own research on this subject.

We’ve also seen discussion through numerous roundtables, think-tanks or regulatory hearings. People suggest, "This is the current system, this is the desired system. Here are some things that regulators may want to think through in affecting the disclosure framework of the future. Here is a way to present information, here’s where the current system is either deficient, vulnerable or might be ripe for improvements." And when you start looking at all of this together, as long as the regulations don't preclude you from doing that, you have your blueprint and recipe to do what you want to do.

If you look, for example, of how the New York Times revamped its weekly magazine. The editors looked at certain trends in the market and how people are consuming information now. Then they decided how to change the way their information is presented. You can do it in one cut, or you can do it over time. You also think about how you link your paper version into your online version.

Neri Bukspan

You can think about the corporate communication in the same vein.There’s no mistaking the fact that there's no mandated regulatory impetus to do it, but simply, you would consider your constituency, your consumers, the people who consumed your information, and their needs dictate your actions and lead to change.

FEI Daily: As the number of words decreases in many disclosures, the impetus to offer information through data visualization becomes more important. Do you think that’s true? And if it is true, how advanced are preparers in taking information that they used to put in a paragraph and present it through some sort of visualization?

Bukspan: There's part of your statement that I agree with, and there's part of your statement that I don't necessarily agree with.

First, I disagree with the fact that fewer words promote greater communication efficiency. To me, it's effective use of communication means. And when you think about the management discussion and analysis section in the 10-K, the MD&A, you can use three paragraphs to describe revenue growth, revenue decline, and what the underpinning reasons were.

You can use two paragraphs to discuss market shares by region, or you can have a pie chart, or a waterfall chart to describe it. That will give you exactly the same kind of information or supplemented information. You can use a few crisp bullet points to highlight certain things, versus a mumbo-jumbo of words. So, to me, if writing things effectively using different presentation means to provide crisp results with a reduction of words, absolutely, I'm all for that. If the reduction of words doesn’t leave out key information, I think it may result in great communication effectiveness.

Learn More: FERF Research Preview

The Financial Executive Research Foundation (FERF) is currently working on a report focusing on disclosure effectiveness and a preview of the research is excerpted below. For more information on this report, or ordering other FERF research material, click here.

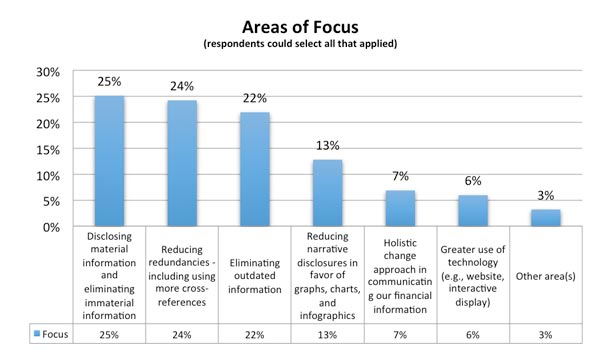

Respondents identified that they are disclosing material information and eliminating immaterial information as their primary focus to improve their financial statements, as well as reducing redundancies – including using more cross references. Other popular areas of focus indicated were eliminating outdated information and reducing narrative disclosures in favor of graphs, charts, and infographics. These focuses where almost identical for private and public companies.

Interviewees agreed with this approach. Most started with the duplication between the MD&A and and footnotes information.

What are the challenges with improving financial disclosures?

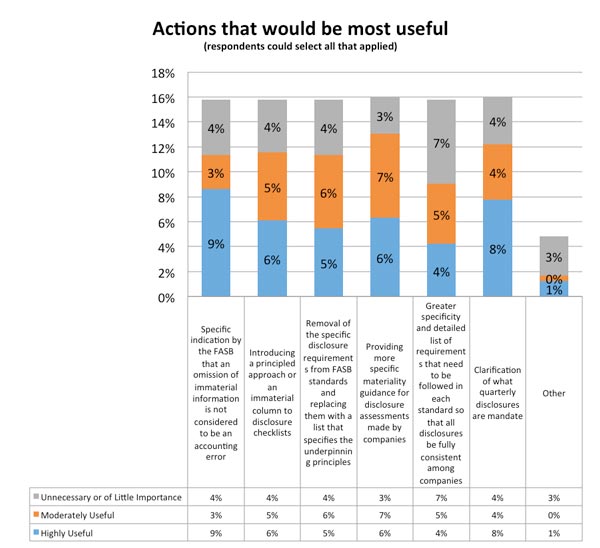

Many respondents suggested that it would be highly useful toremove existing barriers to improvement include FASB or regulatory body indication that an omission of immaterial information is not an error and more guidance on materiality guidelines.

Many respondents suggested that it would be highly useful toremove existing barriers to improvement include FASB or regulatory body indication that an omission of immaterial information is not an error and more guidance on materiality guidelines.