©LDProductions/iStock/Thinkstock

To get it right, XBRL requires involvement from knowledgeable XBRL individuals that have an awareness and understanding of errors beyond what can be caught by software.

For example, below are some errors and the intended meanings that are extracted from quarterly and annual filing. Unless a trained individual is reviewing the filings, these tagging errors may not otherwise be detected:

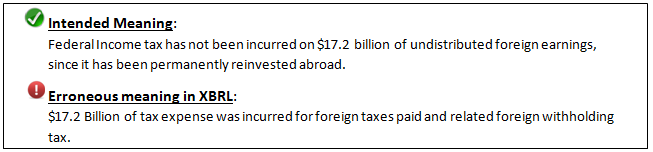

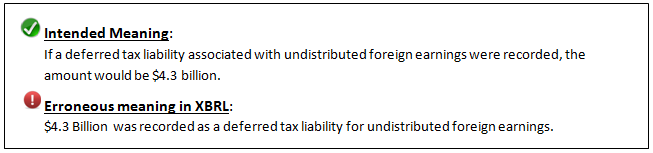

This error was caused by an incorrect usage of an extension, rather than usage of a standard tag in the US GAAP Taxonomy. Another detected mistake within the same file was;

This error was caused by an incorrect usage of an extension, rather than usage of a standard tag in the US GAAP Taxonomy. Another detected mistake within the same file was;

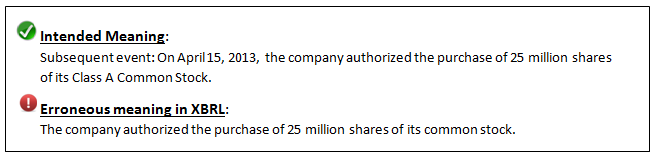

The next error is not necessarily incorrect, it is however incomplete. The company filing this quarterly filing missed the selection of the Subsequent Event member. Also, the classification of the common stock was missing.

The next error is not necessarily incorrect, it is however incomplete. The company filing this quarterly filing missed the selection of the Subsequent Event member. Also, the classification of the common stock was missing.

(To read XBRL Mistakes Really Hurt here)

(To read XBRL Mistakes Really Hurt here)

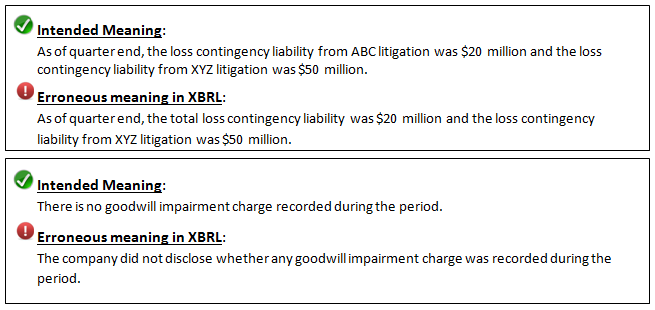

Other examples of where the incorrect tagging will cause the financial to be misrepresented are:

FERF, in collaboration with Merrill Corporation has authored a report on errors undetected by software. The report reveals seven types of XBRL errors that require XBRL knowledge beyond what can be detected by software. Awareness of these error types is key to resolving them and submitting high quality XBRL. The seven are:

FERF, in collaboration with Merrill Corporation has authored a report on errors undetected by software. The report reveals seven types of XBRL errors that require XBRL knowledge beyond what can be detected by software. Awareness of these error types is key to resolving them and submitting high quality XBRL. The seven are:

- The value input into the XBRL document has the incorrect positive or negative sign.

- A new element is created in the US GAAP Taxonomy which should be used to replace an extension tag previously used.

- The tag selected, or the combination of tags selected, represent a different meaning than what is disclosed in the traditional paper-based document.

- An extension is created for an axis element, when an appropriate axis element exists in the US GAAP Taxonomy.

- The structure of the tagging is set up such that the combination of the Axis element and the Member element is inappropriate.

- The same disclosure is repeated within the paper-based financial statements, but different tags are used to tag the disclosure for XBRL purposes.

- The preparer should use the same member element to describe the same category of information shown throughout the paper-based document, but the preparer erroneously uses different member elements to describe the same category of information.

“Submitting high quality SEC XBRL requires an understanding of the issues that create poor quality submissions. Understanding poor quality means knowing about potential errors, not only those that can be detected by software, but those errors that can’t be detected by software,"states Lou Rohman, Vice President of XBRL Services at Merrill Corporation. "Some companies have conquered this and have submitted high quality XBRL, but for the many companies that haven’t, understanding the types of errors that frequently occur is essential to getting it right.”

The good news is there is there is an abundance of information available in the space and more is being added. With each filing event, regulators and filers are gaining awareness and learning more which will ultimately improve the quality of XBRL filings.

To read the full report, please click here Beware XBRL Errors in SEC Filings - Including those Not Detectable By Software