Final standards

Simplifying the accounting for income taxes

On Dec. 18, 2019, the FASB issued ASU No. 2019-12, “Income Taxes (Topic 740): Simplifying the Accounting for Income Taxes,” to reduce the cost and complexity in accounting for income taxes in Topic 740.

The amendments remove the following exceptions from Topic 740:

- Exception to the incremental approach for intraperiod tax allocation

- Exceptions to accounting for basis differences when a foreign subsidiary becomes an equity method investment or a foreign equity method investment become a subsidiary

- Exception in interim period income tax accounting for year-to-date losses that exceed anticipated losses

The amendments simplify and improve guidance within Topic 740 related to:

- Franchise taxes that are based partially on income

- Transactions that result in a step up in the tax basis of goodwill

- Separate financial statements of legal entities that are not subject to tax

- Enacted changes in tax laws in interim periods

- Employee stock ownership plans and investments in qualified affordable housing projects accounted for using the equity method

Effective dates

For public business entities (PBEs), the amendments are effective for fiscal years beginning after Dec. 15, 2020, and interim periods within. For all other entities, the amendments are effective for fiscal years beginning after Dec. 15, 2021, and interim periods within fiscal years beginning after Dec. 15, 2022. Early adoption is permitted.

Narrow-scope improvements to credit losses standard

On Nov. 26, 2019, the FASB issued ASU 2019-11, “Codification Improvements to Topic 326, Financial Instruments – Credit Losses.” The amendments improve certain aspects of the new credit losses standard (ASU 2016-13). The areas of improvement include the following:

- Negative allowance for purchased financial assets with credit deterioration

- Transition relief for troubled debt restructurings

- Disclosures related to accrued interest receivables

- Financial assets secured by collateral maintenance provisions

- Conforming amendment to Subtopic 805-20

Effective dates

For entities that have not adopted ASU 2016-13, the effective dates and transition requirements for ASU 2019-11 mirror the requirements for ASU 2016-13.

For entities that have adopted ASU 2016-13, the amendments in ASU 2019-11 are effective for fiscal years beginning after Dec. 15, 2019, including interim periods within those fiscal years. Early adoption is permitted in any interim period after issuance of ASU 2019-11 as long as an entity has adopted the amendments in ASU 2016-13.

For entities that have adopted the amendments in ASU 2016-13, the amendments in ASU 2019-11 should be applied on a modified retrospective basis by means of a cumulative-effect adjustment to the opening retained earnings balance in the statement of financial position as of the date that an entity adopted the amendments in ASU 2016-13.

Effective dates deferral for major standards for certain entities

On Nov. 15, 2019, the FASB issued ASU 2019-10, “Financial Instruments – Credit Losses (Topic 326), Derivatives and Hedging (Topic 815), and Leases (Topic 842): Effective Dates,” to defer effective dates for the credit losses, derivatives and hedging, and leases standards for certain entities.

The amendments introduce a bucket approach in which effective dates are staggered between larger public companies (bucket one) and all other entities (bucket two). Bucket two entities include private companies, smaller reporting companies (SRCs), not-for-profit organizations (NFPs), and employee benefit plans (EBPs). The board anticipates staggering bucket two effective dates of major updates for at least two years after bucket one effective dates.

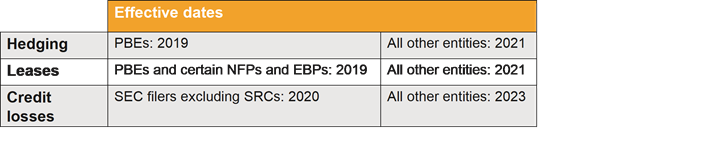

For calendar year-end entities, the following table reflects the effective dates for the major standards:

This ASU also amends the effective date for ASU 2017-04, which eliminated step two from the goodwill impairment test. For PBEs that are SEC filers, excluding entities eligible to be SRCs as defined by the SEC, the amendments in ASU 2017-04 are effective for annual and interim goodwill impairment tests in fiscal years beginning after Dec. 15, 2019. For all other entities, the amendments are effective for annual and interim goodwill impairment tests in fiscal years beginning after Dec. 15, 2022.

Effective date

This ASU was effective upon issuance.

Effective date deferral of long-duration contracts guidance

On Nov. 15, 2019, the FASB issued ASU 2019-09, “Financial Services – Insurance (Topic 944): Effective Date.” This ASU defers the effective date of ASU 2018-12, “Financial Services – Insurance (Topic 944): Targeted Improvements to the Accounting for Long-Duration Contracts,” for all entities.

For PBEs that meet the definition of an SEC filer, excluding entities eligible to be SRCs as defined by the SEC, the amendments in ASU 2018-12 are effective for fiscal years beginning after Dec. 15, 2021, and interim periods within.

For all other entities, the amendments in ASU 2018-12 are effective for fiscal years beginning after Dec. 15, 2023, and interim periods within fiscal years beginning after Dec. 15, 2024. Early application of the amendments in ASU 2018-12 is permitted.

Effective date

This ASU was effective upon issuance.

Improvements to share-based consideration payable to a customer

On Nov. 11, 2019, the FASB issued ASU 2019-08, “Compensation – Stock Compensation (Topic 718) and Revenue From Contracts With Customers (Topic 606): Codification Improvements – Share-Based Consideration Payable to a Customer.” This ASU requires entities to measure and classify share-based payments to a customer by applying the guidance in Topic 718. The amount recorded as a reduction in revenue is to be measured on the basis of the grant-date fair value of the share-based payment in accordance with Topic 718. The classification and subsequent measurement of the award is subject to Topic 718 unless the share-based payment award is subsequently modified and the grantee is no longer a customer.

Effective dates

For PBEs, the amendments are effective for fiscal years beginning after Dec. 15, 2019, and interim periods within. For all other entities that have early adopted ASU 2018-07, the amendments are effective for fiscal years beginning after Dec. 15, 2019, and interim periods within. For all other entities that have not early adopted ASU 2018-07, the amendments are effective for fiscal years beginning after Dec. 15, 2019, and interim periods within fiscal years beginning after Dec. 15, 2020. An entity may early adopt the amendments, but not before it adopts ASU 2018-07.

If an entity adopts the amendments in the same fiscal year that it adopts ASU 2018-07, the entity should apply the amendments in ASU 2019-08 through a cumulative-effect adjustment to the opening balance of retained earnings at the beginning of the fiscal year in which it adopted the amendments in ASU 2018-07.

If an entity adopts the amendments in a fiscal year after the fiscal year that the entity adopts the amendments in ASU 2018-07, the entity should apply the amendments in ASU 2019-08 through a cumulative-effect adjustment to the opening balance of retained earnings at the beginning of either 1) the fiscal year in which it adopted the amendments in ASU 2018-07 or 2) the fiscal year in which it adopts the amendments in ASU 2019-08.

Proposals

Codification improvements

On Nov. 26, 2019, the FASB issued a proposed ASU, “Codification Improvements,” to clarify and simplify a variety of topics. The proposed amendments would result in the following changes to the Accounting Standards Codification (ASC): 1) remove references to various concept statements; 2) relocate disclosure guidance to the appropriate disclosure sections; and 3) various other improvements.

The FASB proposed transition guidance for certain proposed amendments, but other amendments would be effective upon issuance of this proposed ASU.

Comments were due on Dec. 26, 2019.

Transition guidance on reference rate reform

On Nov. 13, 2019, the FASB tentatively approved an ASU that will offer temporary, optional guidance to ease the potential burden in accounting for, or recognizing the effects of, the transition away from the London Interbank Offered Rate (LIBOR) or other interbank offered rate on financial reporting. The ASU is expected to be issued in early 2020. More information regarding the FASB’s reference rate reform project can be found on the FASB website.

To ease the transition to new reference rates, the final ASU will provide optional expedients and exceptions for applying GAAP to contract modifications and hedge accounting relationships that are affected by reference rate reform. The main provisions include:

- A change in a contract’s reference interest rate would be accounted for as a continuation of that contract rather than the creation of a new one for contracts, including loans, debt, leases, and other arrangements, that meet specific criteria.

- When updating its hedging strategies in response to reference rate reform, an entity would be allowed to preserve its hedge accounting.

The guidance is applicable only to contracts or hedge accounting relationships that reference LIBOR or another reference rate expected to be discontinued.

Because the guidance is meant to help entities through the transition period, it would be in effect for a limited time and would not apply to contract modifications made and hedging relationships entered into or evaluated after Dec. 31, 2022.

Improvements to hedge accounting

On Nov. 12, 2019, the FASB issued a proposed ASU, “Derivatives and Hedging (Topic 815): Codification Improvements to Hedge Accounting,” to clarify and improve certain amendments made by ASU 2017-12, “Targeted Improvements to Accounting for Hedging Activities.” The areas of improvement include the following:

- Clarifications regarding change in hedged risk guidance in a cash flow hedge

- Clarifications on the nature of documentation that may evidence a contractually specified component in cash flow hedges of nonfinancial forecasted transactions

- Elimination of recognition and presentation mismatch related to dual hedges caused by ASU 2017-12

- Replacement of term “prepayable” with “early settlement feature” for purposes of applying shortcut method

The proposed amendments would be effective for all entities for fiscal years beginning after Dec. 15, 2020. For PBEs, the proposed amendments would be effective for interim periods within fiscal years beginning after Dec. 15, 2020. For all other entities, the proposed amendments would be effective for interim periods within fiscal years beginning after Dec. 15, 2021. Early adoption would be permitted for all entities on any date on or after the issuance of this proposed ASU if an entity already has adopted the amendments in ASU 2017-12.

Comments were due on Jan. 13, 2020.

Next FASB chair named

Richard R. Jones will be the next chair of the FASB, as announced on Dec. 19, 2019.

Jones will succeed Russell G. Golden when Golden’s appointment ends on June 30, 2020, and Jones is expected to join the FASB early in 2020 to facilitate a smooth transition in leadership. Jones, who has spent his entire career at Ernst & Young, is currently chief accountant and partner in the firm’s national office.